Alberta and Ontario: GDP, Fiscal Balance, and Structural Risk in the Canadian Federation

This blog examines the economic relationship between Alberta, Ontario, and the Canadian federation through the lenses of GDP, sectoral composition, population-adjusted productivity, and federal fiscal flows. While Ontario is Canada’s largest provincial economy in absolute terms, Alberta consistently exhibits significantly higher GDP per capita and a more goods-producing, export-oriented economic structure. Conventional GDP comparisons often obscure these realities by failing to account for structural risks, particularly the inflation of GDP through government spending, housing-linked finance, and population growth.

By contrasting Alberta’s resource-based export economy with Ontario’s finance- and real-estate-heavy service economy, this paper supports the claim that Alberta disproportionately sustains Canada’s fiscal capacity. The analysis concludes by considering the potential implications for federal finances and the Canadian dollar should Alberta become independent.

What GDP Measures, and What It Does Not

Gross Domestic Product measures the value of final goods and services produced within a jurisdiction, but it does not distinguish between market-tested value creation and non-market government output measured at cost. Government output, including public administration and many publicly delivered services, is calculated using input costs such as wages and overhead. As a result, increases in public-sector employment or compensation can mechanically raise GDP even when private-sector productivity remains unchanged.

GDP can also rise through population growth even when GDP per capita stagnates or declines. For this reason, GDP alone is an incomplete measure of economic vitality or sustainability. A more meaningful analysis requires attention to GDP per capita, sectoral composition, the balance between goods and services production, and the net fiscal relationship between provinces and the federal government.

Ontario and Alberta: Scale Versus Productivity

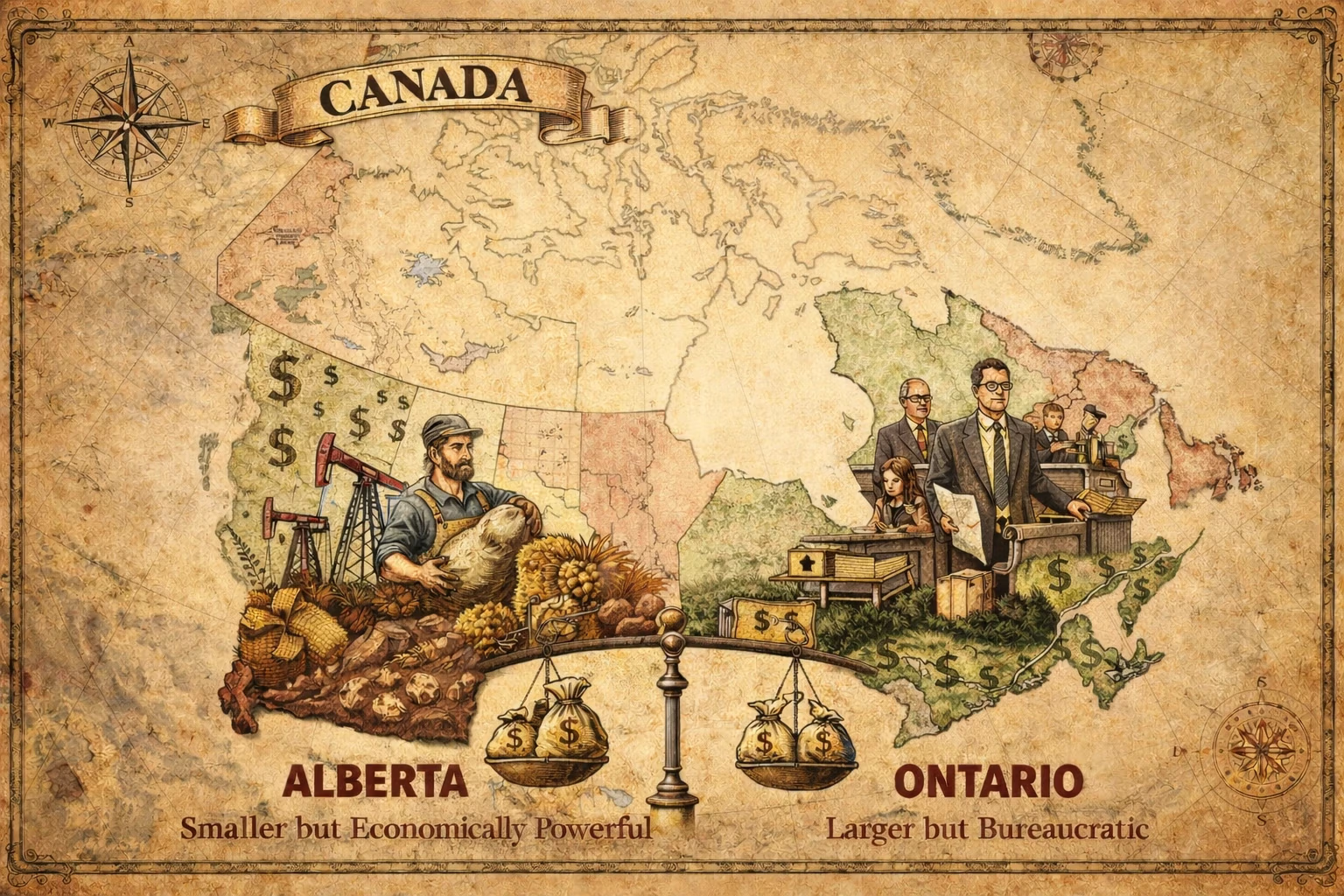

In 2023, Ontario’s GDP was approximately $1.1 trillion, supported by a population of roughly 15.6 million people, yielding a GDP per capita of about $71,700. Alberta’s GDP, by contrast, was approximately $452 billion, with a population of about 4.7 million, producing a GDP per capita near $96,600.

Ontario therefore generates roughly 37 percent of Canada’s total GDP, while Alberta produces approximately 15 percent. However, on a per-person basis, Alberta’s economic output exceeds Ontario’s by roughly 35 percent. This difference highlights the importance of productivity and economic structure rather than sheer population size when assessing economic contribution.

Sectoral Composition and Concentration Risk

Alberta’s economy is heavily goods-producing and export-oriented. Goods-producing industries account for approximately 43 to 44 percent of provincial GDP, with energy and energy-linked industries driving exports, capital investment, and federal tax generation. Alberta’s output is globally priced, trade-exposed, and capable of generating foreign exchange. While energy markets are cyclical, Alberta’s core industries produce tradable goods that sell into global markets and generate external revenues.

Ontario’s economy, by contrast, is predominantly service-based, with services accounting for roughly 77 to 78 percent of provincial GDP. Major components include real estate, rental and leasing, construction, finance and insurance, and professional and administrative services. Approximately 30 percent of Ontario’s GDP is directly or indirectly tied to housing activity, construction, and housing-linked finance. This creates a concentration risk comparable in scale to Alberta’s exposure to energy markets.

The nature of that risk, however, is different. Ontario’s housing-finance complex is domestically leveraged and highly dependent on interest rates, credit expansion, immigration policy, and government backstops. It is not exportable and is not globally priced. A sustained housing downturn could plausibly reduce Ontario’s GDP by 4 to 6 percent over an economic cycle, with spillover effects into construction, banking, consumer spending, and government revenues.

Government Output and GDP Inflation

Ontario’s GDP composition includes a relatively larger share of public administration, government-delivered health and education services, and administrative and regulatory employment. While these activities provide essential services, their inclusion in GDP at cost can inflate measured economic output without corresponding increases in market-tested value creation.

This distinction is important when comparing Alberta and Ontario. Alberta’s GDP is more heavily driven by market-priced goods and exports, while Ontario’s GDP is more sensitive to government spending, housing transactions, and financial intermediation. As a result, headline GDP figures may overstate underlying productive capacity in economies where non-market output and asset-linked services dominate.

Federal Fiscal Balance and Net Contribution

Alberta residents and businesses generate a disproportionately large share of federal personal income tax, federal corporate income tax, GST and excise taxes, and employment insurance premiums. This reflects higher average incomes, higher corporate profitability, and capital-intensive industries.

Alberta retains constitutional control over its provincial resource royalties, which are collected by the Government of Alberta. Ottawa does not receive provincial royalty revenue directly. However, the federal government captures substantial value indirectly through taxation of income and profits generated by Alberta’s resource economy.

On the spending side, Alberta receives significantly less in federal expenditures and major transfers than provinces such as Ontario and Quebec, and it does not receive equalization payments. Over extended periods, Alberta has been one of the largest net contributors to federal finances, meaning that federal revenues collected in Alberta exceed federal expenditures in the province by a substantial margin. This persistent net fiscal imbalance underpins the argument that Alberta disproportionately finances federal programs and redistribution across Canada.

Reframing the “Alberta Is Tied to Oil” Argument

Critics frequently argue that Alberta’s economy is overly dependent on oil and gas. This critique is incomplete. Both Alberta and Ontario exhibit sectoral dependence. Alberta is concentrated in energy and goods production, while Ontario is concentrated in housing, finance, and government-linked services.

The critical difference is structural. Alberta’s anchor industry is export-oriented, globally priced, and revenue-generating. Ontario’s anchor industries are domestically leveraged and policy-dependent. Both carry risk, but only one consistently generates external trade surpluses and foreign exchange.

Implications of Alberta Independence for Canada and the Canadian Dollar

If Alberta were to become independent, Canada would lose a major net fiscal contributor. Federal revenues would decline materially unless offset by higher taxes, increased borrowing, or spending reductions. Federal debt sustainability metrics could weaken as a result.

The impact on the Canadian dollar would depend on several factors, including the continuity of energy exports and investment flows, debt allocation and fiscal adjustment by Canada, and market confidence during negotiations. In the near term, increased volatility, higher risk premiums on Canadian assets, and downward pressure on the currency would be plausible during periods of uncertainty. Long-term outcomes would depend on Canada’s ability to replace lost fiscal capacity and maintain access to Alberta-origin energy exports.

Conclusion

Ontario is Canada’s largest economy by scale, but Alberta is among its most productive and fiscally consequential provinces on a per-capita basis. GDP comparisons that ignore sectoral composition, government output measurement, and federal fiscal balance obscure this reality.

Alberta’s export-oriented, goods-producing economy plays a disproportionate role in sustaining federal revenues and Canada’s trade position. Ontario’s economy, while large, is increasingly exposed to domestic leverage, housing cycles, and government-driven GDP growth. Understanding these structural differences is essential for any serious discussion of fiscal sustainability, federal–provincial relations, or the economic consequences of Alberta independence.

That said, it may be prudent to explore methods by which you can protect your wealth, assuming it’s held in Canadian dollars and assets. Alberta independence is on the horizon, and no matter how much the east says Alberta doesn’t carry the Canadian economy on it’s back- reality will eventually come knocking on Canada’s door and when it does, the loonie will surely tank.

-Christopher Scott